Protect your wealth – for life

The future of retirement is evolving. South Africans are living longer, healthier lives, with many enjoying active lifestyles well into their eighties. This gift of longevity requires an important shift: to build a financial strategy that supports you throughout these extended years, ensuring your wealth works as hard for you in retirement as you worked to build it.

Why smart strategies matter now

The financial landscape offers more opportunities than ever before. With access to global markets, innovative retirement structures like the two-pot system, and sophisticated wealth management tools, today’s investors have powerful options to build resilient portfolios.

The key is understanding how to leverage these tools effectively. The rand’s movements against major currencies, for instance, create opportunities for strategic offshore diversification. In 2024, South African investors increased their offshore allocations by 18% – a savvy move that demonstrates how informed investors are building more resilient, globally diversified portfolios.

The two-pot retirement system brings welcome structured flexibility, allowing you to access funds when you need them while protecting your long-term security. When managed strategically, this flexibility enhances your financial planning without compromising your future.

With the right approach, you can turn market dynamics and economic shifts into advantages. Strategic diversification means your portfolio can benefit from growth opportunities across different asset classes, currencies, and geographies. This isn’t just smart investing – it’s building a foundation that thrives in various market conditions.

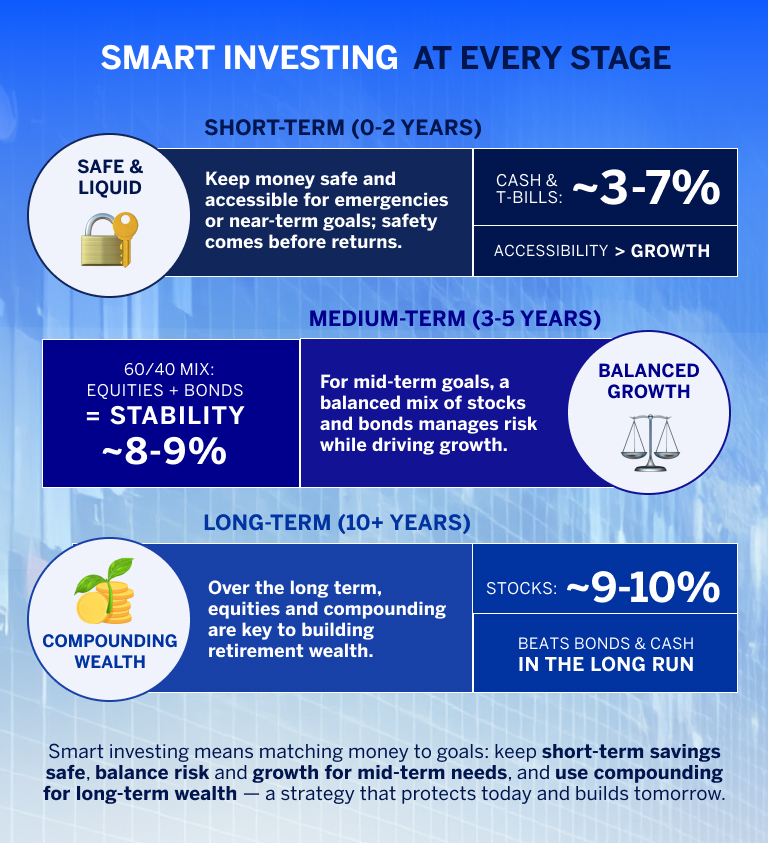

The path to sustainable wealth growth

Successful wealth building is about creating a system that works consistently, delivering results through disciplined strategy rather than speculation. Here is how forward-thinking investors are building wealth that lasts:

Strategic diversification opens doors to global opportunities. By thoughtfully constructing a portfolio that includes international markets alongside local investments, you can access diverse growth opportunities while spreading risk intelligently.

Optimised pension planning ensures every rand works harder for you. Whether you’re maximising tax benefits, strategically planning withdrawals under the two-pot system, or structuring your pension payout for optimal efficiency, the right decisions today can significantly enhance your retirement income.

Inflation protection keeps your wealth growing ahead of rising costs. By including assets that historically outpace inflation, your portfolio maintains and grows its purchasing power over time.

Planning that delivers results

Effective wealth planning starts with clarity. Instead of general goals, successful wealth builders define specific targets: the lifestyle you want to maintain at 65, the experiences you want to enjoy, the legacy you want to create, and the healthcare quality you want to access.

The most robust plans build in flexibility. Life brings opportunities and changes, and your wealth strategy should be designed to adapt and capture upside potential while maintaining core security. This means creating multiple pathways to your goals rather than depending on a single scenario.

Your wealth, your timeline

Your wealth journey is unique, which is why personalised strategies deliver the best results. Your wealth protection plan should be built around your specific situation: your income patterns, your goals, your capacity for risk, and your timeline.

Starting your wealth journey early gives you the advantage of time, allowing returns to compound and smooth out market volatility. Starting later means focusing on efficiency and optimisation. Wherever you are, the principle remains: protecting wealth means managing risk intelligently while capturing growth opportunities.

Suggested benchmark multiples by age

| Age | Multiple of salary you should aim for by this age |

|---|---|

| 25-30 | ~ 1x |

| 30-35 | ~2 - 3x |

| 35-40 | ~3 - 5x |

| 40-50 | ~5 - 7x |

| 50-60 | ~7 - 9x |

| At retirement age (e.g. 65) | ~ 10x or more, depending on lifestyle and expected years of retirement |

(Assumes saving consistently, reasonable investment returns, and moderate inflation.)

How much do you really need to retire?

Understanding your retirement goal starts with one simple question: how much income will you need each month to live comfortably?

The table below translates that monthly lifestyle into the amount of capital you’d need today to sustain it in retirement.

| Consumption expenditure | R12k p/month | R24k p/month | R36k p/month | R60k p/month | R120k p/month |

|---|---|---|---|---|---|

| Before income tax | R12 122 | R27 532 | R44 834 | R84 035 | R188 226 |

| Income before tax to cover 70% consumption expenditure | R17 143 | R34 286 | R51 429 | R85 714 | R171 429 |

| Capital needed today to provide income | R4 198 251 | R8 396 501 | R12 594 752 | R20 991 254 | R41 982 507 |

| Rule of thumb: 30x annual expenses | R4 320 000 | R8 640 000 | R12 960 000 | R21 600 000 | R43 200 000 |

At Standard Bank, we understand that building wealth is as much about preservation as it is about growth. Because the goal isn’t just to accumulate assets – it’s to create the financial foundation that lets you live wealthier, for now and into the future.